Retail

Steady, Not Surging: Canada’s Retail Performance Signals in Winter 2026

March 27, 2026

Calculating time...

Calculating time...

Retail Council of Canada (RCC), in partnership with Moneris Data Services, provides timely credit and debit spending data and consumer insights to help retailers better understand how Canadians are spending—nationally and provincially.

Retail Council of Canada (RCC) draws on a quarterly survey of executives from mid‑ to large‑sized retailers across Canada to provide a directional “retail pulse.” The survey is not statistically representative and excludes gas, motor vehicle, and grocery sectors.

Below is an excerpt from the report covering December 2025 through February 2026.

Key Insights:

Retail Sales and Margins

- About a third of retailers reported lower sales over the period, while 45% posted year-over-year gains. For most, performance was flat to modestly positive — stable, but hardly dynamic.

- Strength of the holiday season:

- Black Friday was the single biggest sales day of the year, with December 22 and 23 reaching 94% and 95% of Black Friday sales respectively — reinforcing the continued strength of physical stores and the role of same-day fulfilment in last-minute gifting.

- Boxing Day has generated no measurable lift to the promotional calendar, consistent with a discounting environment producing stable—not accelerating—returns.

- Margins strengthen:

- 60% of retailers improved margins year over year, driven by tighter promotions, stronger inventory discipline, and more effective supply chain management. While some saw trading down pressure on margins, most are focused on protecting profitability and growing absolute dollars, not margin rates. Cost-cutting alone has largely run its course.

- Basket behaviour tells a clearer story: lower-priced items, greater reliance on deals and private label — classic value seeking behaviour in action.

- The role of premium doorstep delivery:

- While premium delivery services like Instacart and DoorDash may seem at odds with value-focused consumers, they’ve shifted from niche convenience to table stakes. More than half of Canadians have used them, and roughly 90% have access, with frequent usage now common.

- Why the popularity amid value-driven spending? Retailers across formats have partnered with these platforms to compete on same- or next-day delivery using store inventory. Consumers also built the habit through foodservice delivery. For many, there’s a savings logic: lower transportation costs and fewer impulse purchases when sticking to an essentials list.

- Is the Buy Canadian movement still relevant?

- The short answer is yes: Canadians continue to factor country of origin into certain purchasing decisions. The sharp 25% drop in trips to the U.S., alongside increased travel to Europe, Asia and other parts of the Americas, underscores that sentiment.

- Value and affordability still lead. When price and quality are comparable, Canadian products gain an edge — a quiet but meaningful tailwind for domestic retailers

Consumer Behaviour and Spending Trends

- Value shapes the in-store story: Among those tracking store traffic, many reported flat to declining numbers for the period. This is unsurprising given the harsh weather conditions experienced across much of the country, and is not a meaningful cause for concern from a trend perspective. To consumers, physical stores remain an important part of the shopping journey.

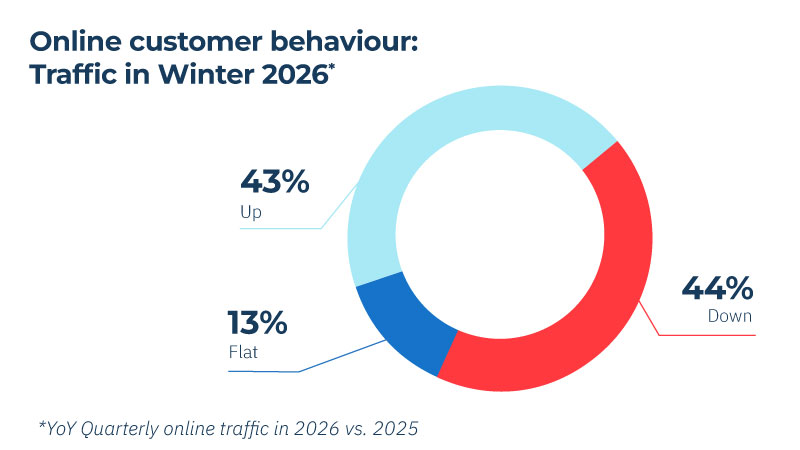

- Online interest, offline purchase: Online, many retailers are seeing impact increase as measured by visitors converting to buyers. The opportunity lies in greater traffic to their sites, and with a unified commerce model of thinking, exposing attribution across all channels and sharper personalization to lift basket size and drive meaningful digital contribution across the enterprise.

- Store consolidation is reshaping shopping patterns: With Nordstrom, Hudson's Bay Company, Peavey Mart and others closing or shrinking, consumers are funneling spending to fewer retailers—especially in mid-market apparel, where department stores once dominated.

Regional Highlights

- Ontario: Continues to lag among most retailers in the country.

- Policy decisions around low priced Chinese EV imports, combined with plant closures, have done little to build confidence in the auto, steel and aluminum sector employees or to encourage big ticket spending.

- Major winter storms in late January and early February suppressed mall traffic and store sales but drove strong demand for seasonal goods and apparel.

- Quebec: Continues to show weaker sales for most retailers.

- British Columbia: B.C. is steady, no longer the growth engine it was in the early part of the decade, with so much consumer spending going into housing.

- Prairies and Alberta: Remain a strong source of strength for most retailers.

- With the federal government making progress on energy and port infrastructure in Alberta and private-sector interest in investments in the Port of Churchill in Manitoba, the outlook remains positive.

- Several retailers report that their sales are stronger in major metropolitan areas than in more rural parts of the three provinces.

- Atlantic Provinces: Remain a strong contributor to retailers of all formats.

- The Carney government’s Defence Industrial Strategy would highlight the significant outlook for the Canadian shipbuilding industry (for example), with benefits continuing to accrue to the Atlantic Provinces.

What are retailers prioritizing for 2026?

The top three initiatives stand out as material priorities shaping retailer strategy in 2026:

- People: Notwithstanding talk of AI taking the place of people, retailers are prioritizing investing in a more agile and productive workforce, both on the front lines and in the offices.

- Store opening and renovations: With several significant brands leaving the Canadian market (Hudson’s Bay, Toys “R” Us, Eddie Bauer), there is a unique opportunity for store expansion and investment. Retailers, however, do not all fit in those boxes, and warn that construction costs and timelines are not in their favour.

- Top line growth: With margins stable but challenging to expand, retailers are growing their top lines to drive returns.

Retailer Sentiment: Steady hands in an unsettled landscape

- Retailers believe they’ve built organizations that are agile, disciplined and able to respond to shocks.

- Where retailers are increasingly concerned is the rise of AI-driven cybercrime on their systems, and, as is often the case, the trajectory of the economy.

- Productivity is chronic and unresolved; tension beneath today’s relative calm.

About Retail Council of Canada

Retail is Canada’s largest private-sector employer with over 2 million Canadians working in our industry. Retail Council of Canada (RCC) is a not-for-profit industry-funded association that represents small, medium, and large retail businesses in every community across the country. As the Voice of Retail™ in Canada, RCC proudly represents more than 45,000 storefronts in all retail formats, including department, grocery, specialty, discount, independent retailers, and online merchants.

Interested in an RCC membership? Please visit here or contact [email protected] for more information.

Author Profile