Consumer Spending Insights

The Index of Consumer Spending reports modest gains in the first quarter of 2026 as labour market experiences losses

May 14, 2026

Calculating time...

Calculating time...

In partnership with Signal49 Research, we’re pleased to share new insights from the Index of Consumer Spending (ICS), powered by Moneris Data Services. By combining our industry‑leading point‑of‑sale transaction data with Signal49 Research’s economic expertise, these insights offer a comprehensive, coast‑to‑coast‑to‑coast view of evolving consumer spending trends in Canada.

Layoffs and global energy disruption cloud Canada's spending recovery

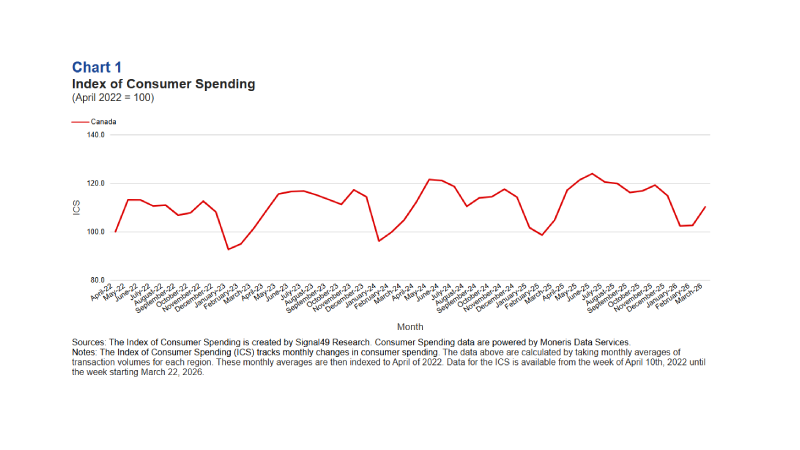

- Signal49 Research’s Index of Consumer Spending (ICS) averaged 105.0 points in the first quarter of 2026 (April 2022 = 100), a 3.3-point nominal increase year-over-year from the 2025Q1 average of 101.7 points. Because the ICS tracks nominal spending, this headline figure includes the effect of price increases.

- After adjusting for the Consumer Price Index, which Statistics Canada reported at an average of roughly 2.2 per cent year-over-year across the first quarter, real consumer spending rose by approximately 1.0 per cent. On a quarterly basis, the nominal ICS declined from an average of 116.9 points in the fourth quarter of 2025, a decrease of 11.9 points, consistent with the seasonal pattern in unadjusted data.

January observations:

- In January, the ICS fell to 102.3 points, a 12.5-point decline from December 2025. A major winter storm from January 23 to 27 disrupted spending across parts of the country, pulling Statistics Canada’s January retail sales figure to 1.1 per cent growth. Unlike in January 2025, the GST/HST was effective on several goods and services that were exempt during the tax holiday a year prior. That added a nominal lift to spending year-over-year, yet ICS growth of 0.7 per cent trailed the 2.3 per cent CPI inflation that Statistics Canada reported for the month, suggesting that real consumer spending contracted on a year-over-year basis. Employment losses also impacted consumer spending. In January, the Labour Force Survey recorded a national employment loss of 25,000 jobs.

February observations:

- In February, the ICS edged up to 102.6 points, a 0.3-point monthly gain but a 4.0-point increase year-over-year, ahead of February’s 1.8 per cent CPI inflation. Statistics Canada noted that the CPI in February 2026 had been pulled down by a base effect from the end of the GST/HST break mid-month in February 2025, so the favourable real reading partly reflects this impact rather than a sincere improvement. Underneath the national reading, the labour market deteriorated sharply. February’s Labour Force Survey recorded a loss of 84,000 jobs.

March observations:

- In March, the ICS surged to 110.2 points, a 7.6-point monthly gain and a 5.4-point increase year-over-year. Following the United States–Israeli strikes on Iran at the end of February, Iran closed the Strait of Hormuz to commercial traffic, disrupting over 20 per cent of global seaborne oil supply. Brent crude prices surpassed $100 per barrel on March 8 and reached as high as $119 per barrel during the month. As gasoline prices rose sharply across Canada, consumers paid more at the pump, adding upward pressure to the ICS. Statistics Canada reported that the CPI in March accelerated to 2.4 per cent year-over-year on the gasoline shock, with gasoline prices up 21.2 per cent on a monthly basis.

- Deflating the nominal ICS by March’s CPI leaves a real year-over-year gain of roughly 2.8 per cent, concentrated regionally in Atlantic Canada. According to our Index of Consumer Confidence, the region showed a notable increase in confidence, even as the national index declined. Supporting the positive momentum, the region received favourable trade news in March, as China lifted its 25 per cent retaliatory tariff on Canadian lobster and crab effective March 1. Nova Scotia’s ICS rose 11.0 points to 121.7, while New Brunswick gained 10.2 points to 119.0, and Newfoundland and Labrador added 10.1 points to 107.4.

Monetary policy was stable throughout the quarter.

- The Bank of Canada held its policy rate at 2.25 per cent at both its January 28 and March 18 meetings, citing heightened risks from U.S. tariff threats and the ongoing renegotiation of the Canada–United States–Mexico Agreement. The policy rate sits 50 basis points below where it was at the end of the first quarter of 2025, but the quarter-long pause in 2026 contrasts with the easing cycle that was underway a year ago. At its March announcement, the Bank noted that rising global energy prices had already affected gasoline costs and were expected to push CPI inflation higher in the coming months should conflict in Iran persist.

Key Insights

Once inflation is netted out, the year-over-year gain in consumer spending is much more modest than the nominal headline suggests.

- The nominal ICS averaged 3.3 points, or 3.2 per cent, above the first quarter of 2025, but Statistics Canada’s CPI rose at an average of roughly 2.2 per cent year-over-year across the quarter, leaving real growth of around 1.0 per cent. Even that modest real gain was concentrated in March rather than spread across the quarter.

- In January, nominal ICS growth of 0.7 per cent fell short of the 2.3 per cent CPI inflation, suggesting real consumer spending contracted year-over-year.

- Two nominal effects explain the gap between headline and underlying demand. First, the reinstatement of the GST/HST implies January 2026 transactions carried a tax-inflated value that was partly absent in January 2025, when the tax holiday ran through mid-February. And second, the March Strait of Hormuz closure lifted recorded fuel transaction values at every pump.

The composition of the labour market helped lessen the spending impact of the sharpest employment contraction since 2022.

- The cumulative 109,000 jobs lost in January and February was the steepest two-month contraction since early 2022 and nearly erased the employment gains of the prior two quarters, yet the national ICS held steady in February.

- Compositional factors in the labour market help explain the gap. Losses were concentrated among youth, part-time workers, and lower-wage service roles (demographics with lower disposable income and spending power), leaving the incomes of higher-paid full-time workers relatively intact.

- Wholesale and retail trade led February's sectoral declines with 18,000 jobs lost, extending a cumulative loss of 52,000 positions since October. Average hourly wages rose 4.7 per cent year-over-year in March to $37.73, partly reflecting the disproportionate share of lower-paid workers among those who left employment. Employment partially rebounded in March with a gain of 14,000 jobs and the unemployment rate held at 6.7 per cent.

About Signal49 Research:

Signal49 Research is Canada’s leading independent research organization. Our mission is to empower and inspire leaders to build a stronger future for all Canadians through our trusted research and unparalleled connections.MONERIS and MONERIS & Design are registered trademarks of Moneris Solutions Corporation. All other marks or registered trademarks appearing on this page are the property of their respective owners.

Author Profile