Consumer Spending Insights

The Index of Consumer Spending slips further in the fourth quarter of 2025 stabilized by holiday activity

March 05, 2026

Calculating time...

Calculating time...

In partnership with Signal49 Research, we’re pleased to share new insights from the Index of Consumer Spending (ICS), powered by Moneris Data Services. By combining our industry‑leading point‑of‑sale transaction data with Signal49 Research’s economic expertise, these insights offer a comprehensive, coast‑to‑coast‑to‑coast view of evolving consumer spending trends in Canada.

November takes the lead in holiday spending

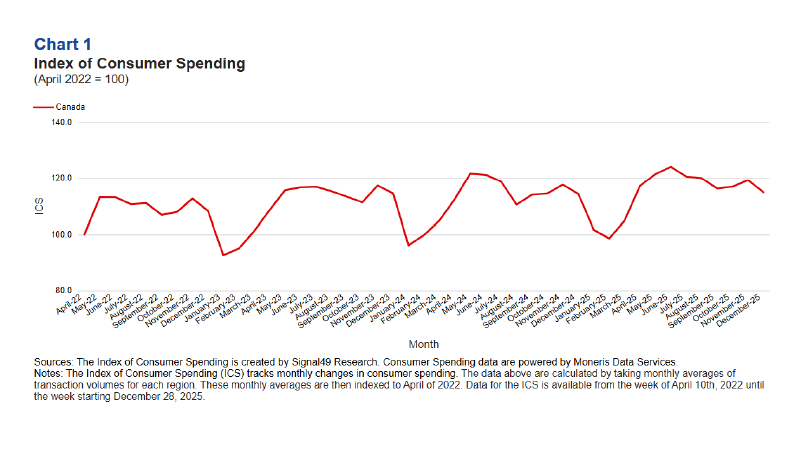

- Signal49 Research's Index of Consumer Spending (ICS) averaged 116.9 points in the fourth quarter of 2025 (April 2022 = 100). Quarter-to-quarter, the ICS declined from an average of 118.8 points in the third quarter, a decrease of 1.9 points, or 1.6 per cent. The results indicate a modest loss of spending momentum heading into year-end.

October observations:

- In October, the ICS reached 116.8 points, increasing 0.7 points from September. Spending strengthened in Quebec and Ontario, where the ICS rose 2.2 per cent and 0.9 per cent, respectively.

- Gains across Canada’s larger provinces offset declines in Prince Edward Island (down 9.6 per cent) and Yukon (down 9.1 per cent) which likely experienced a withdrawal of tourism-driven spending after the summer months.

November observations:

- In November, Canada's ICS rose to 119.2 points, a 2.4-point monthly increase and the strongest gain of the quarter.

- Statistics Canada's retail trade data show that retail sales increased 1.3 per cent month over month in November. Spending around Black Friday and Cyber Monday contributed to a large volume of transactions throughout the month.

- In addition to stronger discretionary spending, higher inflation in household staples also provided a lift to November's ICS score. Grocery prices rose 1.9 per cent from October to November, the largest month-over-month increase since January 2023, driven by sharp increases in beef and coffee.

- Labour market improvements also supported stronger spending. In November, employment rose by 54,000 jobs, driven almost entirely by gains in part-time work and seasonal hiring, while the unemployment rate fell to 6.5 per cent.

December observations:

- Finishing the year and the quarter, December's ICS fell to 114.8 points, a 4.4-point decline from November. Statistics Canada's advance estimate indicates that retail sales declined 0.5 per cent in December, following the 1.3 per cent gain in November. This pattern is consistent with a pull-forward of holiday purchases into November.

- Provincial declines were widespread in December’s ICS, including 5.8 points in Ontario, 5.4 points in Quebec, 9.0 points in Nova Scotia, and 6.8 points in New Brunswick. Underlying economic conditions likely constrained December's performance.

- According to Statistics Canada's December Labour Force Survey, the national unemployment rate climbed to 6.8 per cent, and employment gains were muted through the month with just 8,200 positions added on net.

- Monetary policy was generally stable over the quarter. The Bank of Canada held its policy rate at 2.25 per cent in December 2025, following two earlier cuts in September and October that had reduced the overnight rate by a cumulative 50 basis points. Those earlier cuts helped ease some of consumers’ debt-servicing burdens, particularly for variable-rate mortgage holders. Given elevated essential costs and debt, the rate relief likely had a limited effect on discretionary spending in the fourth quarter.

Key Insights

Holiday spending continues its trend towards November with households completing a significant share of holiday purchases during the Black Friday and Cyber Monday period.

- This trend has been building for nearly two decades and has accelerated with the rise of online shopping, which now accounts for nearly 12 per cent of retail sales compared with less than 4 per cent a decade ago.

- This is also supported by a 2025 survey by the Retail Council of Canada which found that 84 per cent of Canadians view Black Friday as the most important shopping day of the year. For retailers and policymakers, this means that November has become the critical month for assessing holiday performance, while December has growingly become residual activity rather than the main seasonal peak.

- Essential cost pressures are reshaping the composition of nominal spending. Across the quarter, food inflation played a central role in shaping nominal spending. In November, grocery prices rose 1.9 per cent from October, the sharpest monthly gain since January 2023. Combined with housing and other fixed costs, these pressures pushed a larger share of total spending into essential categories. This limited the potential upside of holiday spending.

Labour market and policy conditions are acting as a stabilizing force rather than a catalyst.

- The fourth quarter’s labour market and policy backdrop acted as a floor rather than a driver of consumer spending. Stronger employment gains in October and November along with modest wage growth provided some support while at the same time, and the Bank of Canada's decision to hold the policy rate at 2.25 per cent after earlier cuts stabilized borrowing costs. Despite these generally positive trends, consumer spending remains constrained by weak confidence driven by ongoing economic uncertainty.

About Signal49 Research:

Signal49 Research is Canada’s leading independent research organization. Our mission is to empower and inspire leaders to build a stronger future for all Canadians through our trusted research and unparalleled connections.

Author Profile